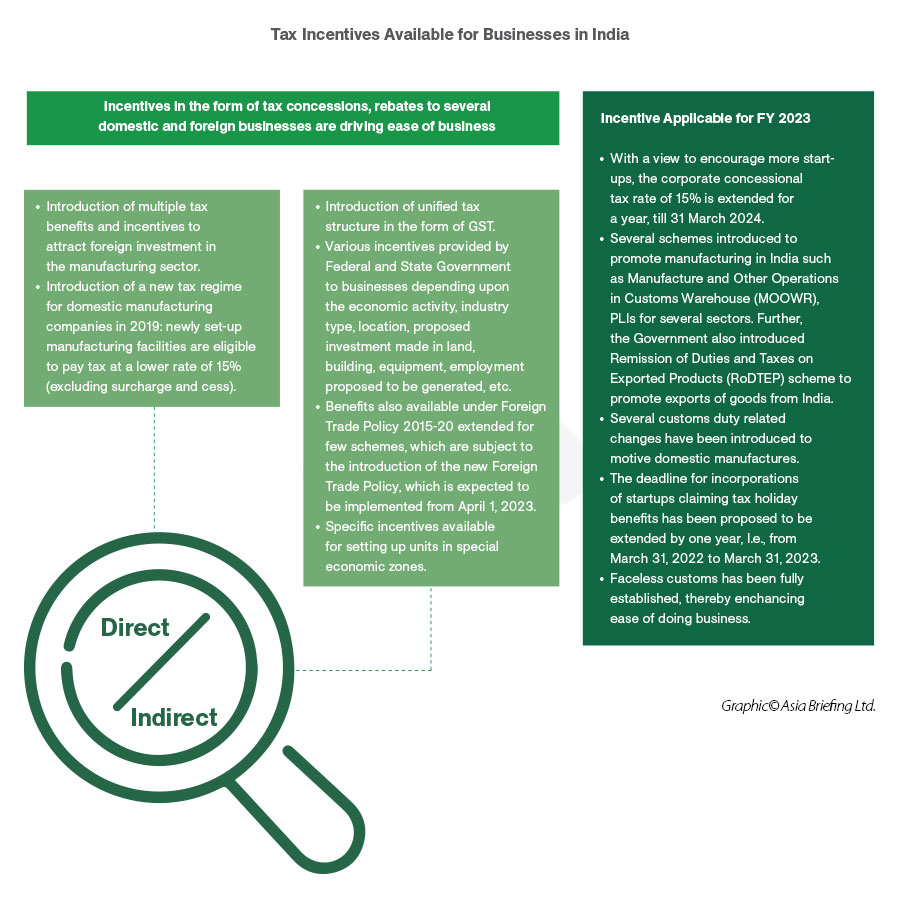

Tax incentives are available to businesses in India depending on the economic activity, industry, location, and size of the firm.

Investors become eligible for most of India’s tax breaks and incentives after registering with the Ministry of Corporate Affairs. Tax incentives tied to specific targets – such as hiring over 50 Indian employees – often require additional permissions from related ministries.

India offers tax relief at both the central and state level. Additional incentives are available to investors in specific sectors, while India’s special economic zones (SEZs) offer their own comprehensive tax relief. However, not all tax benefits offered in India are mutually inclusive.

For tax incentives issued by individual states, the related state’s directorate of industries is usually the body in charge of granting benefits.

Production-linked incentives (PLI) to boost manufacturing

The government has rolled-out targeted production-linked incentive (PLI) schemes to select beneficiaries in specific sectors.

Applicants from both local and foreign firms will benefit from PLI incentives in each sector.

The following sectors have been identified as intended beneficiaries of the PLI scheme with the government allocating budget outlay for the next five years:

- Pharmaceutical sector – the scheme will last for a duration of nine years from 2020-21 to 2028-29 for the purpose of creating a wide range of affordable medicines for local consumers and to move up the global supply chain of medicines. Assigned a budget outlay of US$2.04 billion;

- Medical devices sector – to create local domestic manufacturing capacity and promote medical device parks, the PLI scheme’s target segments include manufacturing radiology and imaging medical devices, anesthetics, and cardio-respiratory medical devices, etc. Assigned an outlay of about US$472 million;

- IT sector – to support the goal of becoming a global supplier of information technology (IT) hardware, the government will provide the sector with an incentive on net incremental sales of goods manufactured during a four-year period. Assigned an outlay of about US$1 billion;

- Advance chemistry cell (ACC) battery sector – will be reportedly aided in incentivizing large domestic and global companies to contribute towards making the sector more competitive within India itself. Assigned outlay of US$2.46 million;

- Automobiles and auto components sector – will be reportedly aided in becoming more globally competitive. Assigned outlay of US$7.7 billion;

- Telecom and networking products sector – will be reportedly aided in attracting large foreign investments that will help domestic companies emerge in the global export market. Assigned outlay of US$1.6 billion;

- Technical textiles and textile products in the man-made fiber (MMF) segment – will be aided in attracting large investments to boost domestic manufacturing. Assigned outlay of US$1.4 billion;

- Solar photo-voltaic (PV) modules sector – will be aided in incentivizing domestic and global companies to build the capacity for large-scale solar PV module manufacturing and then assimilate into its global supply chain. Assigned outlay of US$613 million;

- Specialty steel sector – will be aided in enhancing the manufacturing of value-added steel that will be then expected to raise its total exports. Assigned outlay of US$861 million; and

- Food products sector – will be aided in identifying the specific food products whose production will be able to bring in medium-to-large-scale employment (refers to employing between 50-250 persons). Assigned outlay of US$1.48 billion.

Incentives for electronic manufacturing in India

Scheme for Promotion of Manufacturing of Electric Components and Semi-Conductors (SPECS) in India (2020):

|

Target Segment |

Incentive |

Eligibility |

Tenure |

Status |

|

Components and Semiconductor |

Financial inventive of 25% of the capital expenditure incurred for the manufacturing of specified components and semiconductors. |

Investments in new and expansion of capacity / modernization and diversification of existing units with minimum investment threshold ranging from INR 5 crore to INR 1,000 crore |

Open for applications for a period of 3 years from notification i.e., till 31 March 2023. Benefits will be available for a minimum investment made within 5 years from the date of acknowledgement of the application. |

In progress |

PLI for Large Scale Electronics Manufacturing in India (2020):

This scheme provides incentive of four to six percent on incremental sales (over base year FY 2019-20) of goods manufactured in India for a period of five years. The eligible companies will belong to target segments, such as mobile phone and specified electronic components manufacturing. This also covers assembly, testing, marking, and packaging (ATMP) units.

|

Production-Linked Incentive Schemes in India: Target Sectors and Incentives |

||

|

Sectors |

Incentives |

|

|

1 |

Mobile manufacturing and specified electronic components |

|

|

2 |

Manufacturing of medical devices |

|

|

3 |

Critical key starting materials (KSM) / drug intermediaries (DI) and active pharmaceutical ingredients (API) |

|

|

4 |

White goods (ACs and LEDs) |

|

|

5 |

Telecom and networking products |

|

|

6 |

Electronic/technology products |

|

|

7 |

Pharmaceuticals drugs |

|

|

8 |

Food products |

|

|

9 |

Solar PV modules |

|

|

10 |

Advanced chemistry cell (ACC) battery |

|

|

11 |

Textile products |

|

|

12 |

Automotive industry and drone industry |

|

|

13 |

Specialty steel |

|

Modified Electronics Manufacturing Clusters Scheme (EMC 2.0):

|

Target Segment |

Incentive |

Eligibility |

Tenure |

Status |

|

Development of world class infrastructure along with common facilities and amenities through Electronics Manufacturing Clusters (EMCs) |

Financial assistance:

|

Land Requirements

Anchor Units

EMC Expansion

CFC in existing EMC Projects

CFCs Expansion

|

Open for receipt of applications for 3 years (i.e., up to 31st March 2023). Notified on 1st April 2020 with an implementation period of 8 years |

In progress |

Manufacturing and Other Operations in a Customs Bonded Warehouse (MOOWR)

Central Board of direct Taxes & Customs (CBIC) launched MOOWR to defer the Customs duties on imported goods that are used for the intended purposes of manufacture or carrying out other activities.

Types of businesses covered: Any business desiring to conduct manufacture or any other operations can apply under MOOWR. Existing businesses can also apply.

Sourcing of capital goods and inputs: MOOWR gives flexibility in sourcing capital goods as well as inputs. The capital goods and inputs can be sourced through imports, domestic market or even from SEZ/ FTWZ.

Full flexibility in clearance of finished goods: The goods produced under the scheme can be exported or cleared to domestic market as per demand. No export obligation is prescribed.

Duty benefits: MOOWR is a duty deferment scheme and not a duty exemption scheme. The duty on both imported capital goods and inputs stands deferred till their clearance from warehouse. In case of clearance of capital goods to DTA, deferred duties will become payable. In case of clearance of finished goods into DTA, GST on finished goods along with import duties on imported inputs are payable. The GST as well as the IGST paid as part of import duties will be available as credit. In case of export of capital goods or finished goods, the duty on imported inputs stands remitted. Also, zero rating of tax on domestic inputs is allowed.

MSME friendly: MOOWR does not have minimum investment requirement or restriction on its location. Coupled with the flexibility of sourcing capital goods and inputs, and flexibility for sale, the scheme is suitable for MSMEs.

Incentives for Special Economic Zones (SEZs)

Incentives for SEZs to enhance exports from and promote FDI in India, include:

- Relaxation of payment of customs and excise on imports from domestic sources;

- Tax holiday for SEZ developers;

- Tax exemption for offshore banking units in SEZ;

- Exemption from minimum alternate tax;

- Exemption from capital gains tax – the exemption is available, if within one year before or three years after such transfer:

- Machinery or plant is purchased for the purposes of business of industrial undertaking in SEZ by the assessee;

- The assessee has acquired land or building or has constructed building for the purposes of business in SEZ;

- The original assets are shifted, and establishment of the industrial undertaking is transferred to SEZ, and other specified expenses have been incurred; and

- The amount of exemption for capital gains is restricted to the costs and expenses incurred in relation to all or any of the purposes mentioned above.

Conditions for SEZ developers

To avail incentives, the firm must:

- Be involved in the development, operation, and maintenance of SEZs, including their infrastructure facilities;

- Be engaged in the export of goods and services from April 1, 2005 onward;

- Not be formed by splitting up or reconstructing an existing business; and

- Not to be formed by transferring a previously owned plant and machinery to the SEZ unit.

Incentives for startups

Tax incentives are granted to startups that are considered eligible under the government’s ‘Startup India’ plan. 31 of the 36 Indian States and Union Territories have a dedicated Start-up Policy.

New businesses should meet the following conditions to be eligible under this plan:

- A company that has been incorporated for less than seven years qualifies as a startup. For a company operating in the biotechnology sector, this time period is 10 years;

- The annual turnover of the company should not be more than INR 1 billion;

- The company should aim towards development, innovation, deployment, or commercialization of any new products, services, or processes that are either driven by technology or intellectual property;

- The company cannot be created by splitting up or restructuring an existing company;

- The company has to get its certification from the Inter-Ministerial Board setup; and

- The company can be registered either as an LLP, registered partnership or a private limited company.

An entity will not be considered a startup after:

- Completion of ten years from the date of its incorporation/registration, or

- Achieving turnover of more than INR 100 crore in any previous year.

Incentives and tax exemptions for the eligible startup in India

- Any startup incorporated till March 31, 2024, can get a 100 percent tax rebate on its profits for a total period of three years within a block of ten years. However, if the company’s annual turnover exceeds INR 1 billion, then the tax rebate is not valid;

- These startups are exempt from long-term capital gains tax. However, this is only applicable if the capital gains that have been invested are a part of the fund notified by the central government within a total period of six months from the date of the actual transfer of the asset; and

- If an eligible startup makes an investment, the government will exempt the tax on the investment above the fair market value. This includes a range of different investments, such as funding secured by resident angel investors, and funds that are not registered as venture capital ones. Investments that are made by incubators above the fair market value are also exempt under this plan.

Other incentives:

- India allows startups to convert debt investments made into company equity shares for up to 10 years to ease pressures from the COVID-19 pandemic on entrepreneurs.

Tax incentive of capital expenditure on certain specified businesses

100 percent deduction of capital expenditure is allowed in the year when the commercial operations begin for the following specified businesses:

- Setting up and operating cold chain facilities;

- Setting up and operating warehousing facilities for storage of agriculture produce;

- Setting up and operating an inland container depot, freight station, or warehousing facility for storage of sugar, beekeeping, and honey and beeswax production;

- Laying and operating a cross-country natural gas or crude or petroleum oil pipeline;

- Network for distribution, including storage facilities being an integral part of such a network;

- Building and operating a hotel of two-star or above category in India;

- Building and operating a hospital with at least 100 beds;

- Developing and building a housing project under a scheme for slum redevelopment or rehabilitation framed by the government;

- Developing and building specified housing projects under an affordable scheme of the central/state government; and

- Investing in a new plant or newly installed capacity in an existing plant for production of fertilizer.

Corporate tax incentives for eligible companies

Domestic (locally incorporated) companies can opt for a 22 percent CIT rate and new domestic manufacturing companies, 15 percent. Choosing the concessional regime would require meeting certain specified conditions.

Domestic companies

The concessional tax regime for domestic enterprises if they do not avail of specific tax incentives or deductions is 22 percent. The effective tax rate for these domestic companies is around 25.17 percent inclusive of surcharge and cess.

Those companies opting for the concessional corporate tax rate do not have to pay minimum alternate tax, which is at par, on average, with leading Asian investment destinations and manufacturing hubs like China, Vietnam, Malaysia, Singapore, and South Korea.

There is no restriction on company turnover to be eligible for choosing the concessional regime and the company need not be a new company; any existing company can migrate to this regime at any point. Once the domestic company chooses the new tax rate in a particular financial year – they cannot subsequently opt out.

New domestic manufacturing companies

If a new domestic company is engaged in the business of manufacture or production of any article or thing, or research in relation to such article or thing, or engaged in the distribution of such article or thing manufactured or produced by them – they can claim the benefit of section 115BAB.

The eligible manufacturing company can exercise the option to be taxed under section 115BAB on or before the due date of filing income tax returns, which is September 30 of the assessment year, unless extended. Once the company opts for section 115BAB in a particular financial year, it cannot be withdrawn subsequently.

Eligibility

- The company was set up and registered on or after October 1, 2019 and commenced manufacturing on or before March 31, 2023;

- The company must not be formed by the splitting up and reconstruction of an already existing business – except in the case of a business that is re-established under section 33B, Income Tax Act;

- The company does not use any previously used (second hand) plant or machinery for any purpose. However, the company can use plant and machinery that was used outside India and is now being used in India for the first time. Also, the company can use old plant and machinery, if their value does not exceed 20 percent of the total value of the plant and machinery used by the company; and

- The company does not use a building that was previously used as a hotel (two-star, three-star, or four-star category as classified by the Central Government) or a convention center.

Tax incentives in different Indian states

Foreign companies choosing where to set up in any of India’s states should note that each region has its own set of policies and incentive schemes. The applicability of incentives usually varies based on:

- The state’s location;

- The products that will be manufactured;

- The scale of investment; and

- The creation of jobs.

Incentives for capital investment could include reimbursement in the form of subsidies (capital and interest subsidy, land rebate). Incentives to relieve burden on expenditure incurred could include exemptions on government payments for electricity duty, stamp duty, and external development charges as well as reimbursement in the form of employment generation subsidies. States may also provide GST subsidy on sales made through GST refund and/or investment promotion subsidy.