Op-Ed Commentary: Chris Devonshire-Ellis

Oct. 14 – As China becomes increasingly shrill in its condemnation of the prospect of a U.S. default, an interesting question begins to arise – which Asian economies could withstand such an event? Xinhua, China’s official government news agency, said that as American politicians continued to flounder over a deal to break the impasse, “it is perhaps a good time for the befuddled world to start considering building a de-Americanized world.”

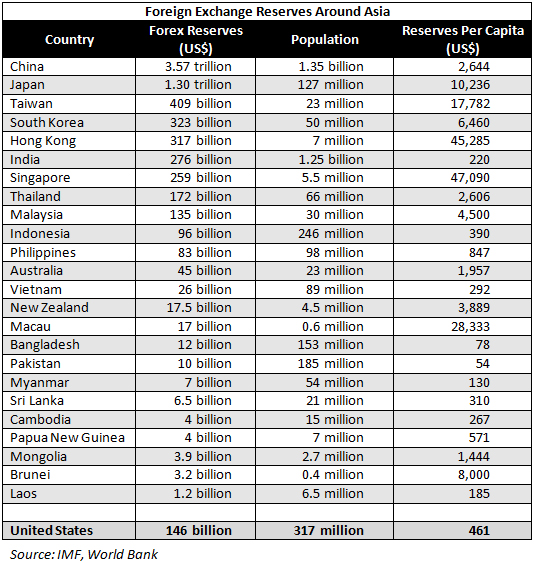

China would say that – it holds over US$1.6 trillion of U.S. treasury bonds, by far the largest of all American creditors. It has also been quietly building up currency swap relationships with other countries, and has signed off about US$400 billion in swap lines with more than 20 foreign banks since 2008. The latest of these was with the Indonesian rupiah last week. To put the issue concerning foreign exchange reserves into context, Indonesia’s US$96 billion would be enough to cover the cost of imports into the country for five months. Indonesia’s population is just under 250 million.

Yet other Asian nations have also been prudent when it comes to managing their finances. Moody’s just upgraded the Philippines’ credit status to investment grade after praising the countries fiscal policies, and in total, Asian nations from South Korea to Pakistan have amassed over US$6 trillion of foreign exchange reserves. Reuters, who track foreign exchange reserves of 12 Asian nations, has indicated that this continues to rise; another US$85.6 billion was added to Asian reserves in the past quarter.

“The level of external reserves of Asian countries continues to be healthy,” Philippines Central Bank Governor Amando Tetangco said last week. “We are in a better position to meet the challenges that may be brought about by external shocks. But we need to remain vigilant.”

Asian governments have been reducing their debt and forging bonds through swap agreements over the past few years which allows them to borrow from their neighbors’ reserves. Curiously though, although roughly three-fifths of all Asian savings are in U.S.-backed securities, the effect of any potential default or liquidity problems is to send money spinning out of foreign currencies and into the U.S. dollar to keep it afloat. This happened earlier this year in both India and Indonesia, when strong capital outflows as a result of bad news from Washington meant both countries had to raise interest rates to protect that, yet at the same time incurring a commercial financial penalty – as doing so hurts growth. This occurred despite the fundamentals for both countries being strong – and also added further credibility to China’s voice for the world to de-link from the U.S. dollar.

As can be seen, several Asian countries have impressive reserves – and China, Japan, Taiwan, India, South Korea, Singapore, Thailand and Hong Kong all have higher foreign reserves than the United States itself. While that may not be surprising given that the greenback is the dominant currency, it does signal that in the call for a better spread of currencies, the United States has a lot of work to catch up in terms of spreading risk should the global financial picture begin to diversify.

Of note too is the correlation between a nation’s reserves and its population. With reserves being earmarked for national savings, in the event of a crisis, these would also be needed to pay for imports, primarily of foodstuffs and energy, to keep the population going. It is very hard to draw comparisons here, as many Asia nations are major producers of food and have more than enough. China, however, is a major importer. That said, the nations with the highest ratio of reserves per capita make interesting reading: relatively small enclaves such as Singapore, Hong Kong and Macau are way out on top, while in the medium-populated country stakes, Japan, South Korea, Malaysia and Thailand all look secure. India, Indonesia and Vietnam appear low in per capita rankings but all are major food producers and export large quantities of staples. China’s figures appears healthy, however, the country is not self-sufficient and has some risk. Lower down the scale, poorer nations with high populations and low reserves are at the greatest risk – Bangladesh, Pakistan looking especially vulnerable.

While I think the prospect of a U.S. default is unlikely, the situation has highlighted an important subject: the over-reliance on the United States as the holding currency of first resort. With the U.S. embroiled in highly partisan and damaging political disputes, and economically not in the best of health, calls for a reserve currency will increase. The Euro – which was intended to fulfill that role – is mired in its own problems with the imposition of a single currency unit covering both the wealthy northern European nations as well as the poorer southern Europeans, while China, to be frank, doesn’t have the economic strength either, despite its rhetoric. What will happen I suspect is that while the dollar will remain dominant, the move to arrange swap lines of credit between developing currencies such as the RMB, the Russian ruble and possibly even the India rupee will continue, and countries in Asia will save less U.S. dollars and more of each other’s currencies to hedge against the current politically unstable position of American politics – and the impact of that upon American securities.

Editor’s Note (Oct. 14, 2013): South Korea and Indonesia have just announced a US$10 billion currency swap deal, bringing the amount of such deals Indonesia has engaged in this year to US$35 billion.

Chris Devonshire-Ellis is the Founding Partner of Dezan Shira & Associates – a specialist foreign direct investment practice providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in emerging Asia. Since its establishment in 1992, the firm has grown into one of Asia’s most versatile full-service consultancies with operational offices across China, Hong Kong, India, Singapore and Vietnam as well as liaison offices in Italy and the United States.

For further details or to contact the firm, please email asia@dezshira.com, visit www.dezshira.com, or download the company brochure.

You can stay up to date with the latest business and investment trends across Asia by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.