Nov. 18 – The International Monetary Fund (IMF) has concluded its annual Article IV Consultations with Singapore, Thailand, and the Republic of Korea. Conducted annually, Article IV Consultations attempt to assess each country’s economic health and forestall future financial problems.

The results of the three Consultations were inevitably mixed.

In its report on Singapore, the IMF called upon the country to narrow its current account surplus and embraced government plans to increase public spending on infrastructure and social services. It additionally characterized the country’s financial sector as well-regulated and highly developed. Its report on South Korea was similarly supportive and stated that “many of the [economic] reforms needed…are already in train or planned.”

Its report on Thailand, however, was slightly more contentious and even provoked a rebuke from the Thai government. Finance Minister Kittiratt Na-Ranong lashed out at the IMF on Wednesday saying that “the IMF should try to understand Thailand’s situation better before giving out suggestions. We listened to different points of view but the IMF needs to profoundly understand the situation before giving theoretical comments.”

The IMF’s report on Thailand advised the country to raise its value-added tax from 7 to 10 percent and suggested the Bank of Thailand increase its policy rate to reduce the impact of inflation, among other things.

Summaries of the IMF’s key findings and recommendations can be found below.

Singapore

Since Singapore’s rapid and robust recovery from the global financial crisis, the city-state’s growth momentum has slowed and become increasingly erratic. Growth slowed to 1.25 percent in 2012 before picking up again in the first half of 2013. Projections indicate that growth will likely reach 3.5 percent in 2013-2014, but be accompanied by a rise in core inflation.

Unsurprisingly, Singapore’s financial regulation and supervision frameworks were rated among the best globally, and stress tests indicated financial institutions would have no problem coping with adverse developments such as a sharp drop in property prices.

The IMF did recommend, however, that Singapore narrow its account surplus, allow the local dollar to rise at a faster pace to aid external rebalancing, and closely monitor the rapid growth of credit and real estate prices. This rapid growth, according to the report, makes the country’s economy increasingly sensitive to macroeconomic shocks and interest rate cycles.

Other suggestions included Singapore imposing a counter-cyclical capital buffer on banks, stepping up its monitoring of bank credit risks and foreign currency liquidity practices, ensuring the banking industry adequately contributes to the cost of resolving failed banks, and further developing recovery plans for the Singapore Exchange (SGXL.SI).

A number of other downloadable topic-specific reports have also been released recently by the IMF:

- Singapore: IMF Selected Issues

- Financial System Stability

- Observance of Standards and Codes

- The official press release, including selected economic and financial indicators (2008-14), can be accessed here.

Thailand

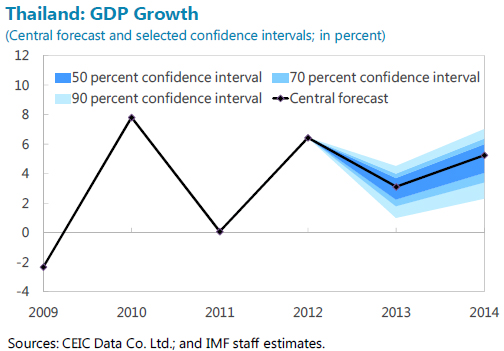

Overall, the Thai economy has demonstrated an incredible resilience to large shocks such as the global financial crisis, supply-chain disruptions following the tsunami in Japan, and devastating floods in late 2011. This resilience is partly attributable to governmental efforts to diversify drivers of economic growth (including redistribution policies to boost domestic consumption and infrastructure improvement projects to lower logistics costs), further integrate the Mekong Region with South China, and fortify the economy against natural hazards. Volatile capital flows, however, have presented challenges to Thailand’s macroeconomic policy.

In 2012, Thailand’s real GDP grew 6.5 percent, private consumption rose 6.7 percent, and private investment grew by 14.4 percent – a significant rebound after widespread flooding in 2011 stalled growth. In early 2013, however, growth slowed significantly with real GDP declining by 1.7 percent in the first quarter, and 0.3 percent in the second.

The IMF report views external factors as likely to hinder economic growth in the long term. Slower-than-expected growth in China or India is projected to have a major impact on trade linkages and overall GDP growth.

Moving forward, Thai officials must continue to rebuild fiscal buffers, strengthen financial stability, and promote more inclusive growth. While the current accommodative monetary policy stance is viewed as appropriate, authorities must normalize their stance if inflationary pressures re-emerge.

A reversal in capital flows since May can also be checked by Thailand’s strong international reserve position together with exchange rate flexibility and macro-prudential and capital flow measures as appropriate.

The report directed specific criticism at Thailand’s US$21 billion rice-purchasing program, saying that if the program remains unchanged it has the potential to damage confidence in public finances and the economy. Ending the program can also reduce deficit and allow Thailand to meet its goal of a balanced budget by 2017. This is not the first time Thailand’s rice-buying policy has attracted concern, however. Earlier this year, a committee representing the World Trade Organization asked Thailand for more information about the program after the United States, European Union, Australia, and Canada voiced concerns about the program violating domestic support limits.

Key policy recommendations:

- Create fiscal space for priority spending and gradually rebuild policy buffers to prepare for adverse shocks. Strengthen medium-term fiscal framework.

- Allow the exchange rate to continue to move flexibly in line with fundamentals and respond with macroeconomic policies and capital flow measures to deal with capital flow surges.

- Strengthen the regulatory and supervisory framework for specialized and non-bank institutions.

- Implement planned infrastructure investments to enhance competitiveness and promote inclusive growth.

- The official press release, including IMF’s selected financial indicators, can be accessed here.

South Korea

The IMF’s Article IV Consultation on South Korea was optimistic and praised continuing government efforts to balance the nation’s economic structure. The team released the following statement at the conclusion of their visit:

“The Korean economy has fared well in the recent turmoil and is well-positioned to benefit from the global recovery, reflecting strong fundamentals and skilled policy-making. However, it will need to rebalance its economic structure to continue lifting the living standards of its population, in an inclusive way, ever closer to that of the richest advanced economies. Many of the reforms needed, and identified below are already in train or planned. Steadfast implementation across these areas will be needed.”

Highlights include expectations that Korea’s GDP growth will rebound to 2.8 percent in 2013 and inflation will continue to be subdued. In 2014 growth is expected to further strengthen to 3.7 percent, but private domestic demand momentum in the short term is expected to remain relatively weak. While mild turmoil from U.S. monetary policy normalization is unlikely to have a significant impact on the Korean economy, any adverse growth in its main export markets – China, the U.S., and the EU – could seriously damage its 2014 outlook.

South Korea’s financial sector is characterized as very stable, and banks’ vulnerability to external liquidity shocks has declined as macro-prudential regulations have reduced their short-term external debt. In some respects, Korea has emerged as a safe haven of sorts amidst the summer’s market turmoil with low inflation, a strong fiscal position, and ample foreign reserves.

The report recommends that while South Korea’s 2014 budget is well-calibrated, a more counter-cyclical fiscal framework should be adopted that includes a structural balance target. After 2014, the central government could reduce this balance to finance growth-enhancing social spending to help rebalance the economy towards domestic demand.

The IMF argues that considerable productivity gains could be achieved by deregulating network services, education, health, professions, and by promoting competition in service provision to and by conglomerates. Permitting market-base pricing for utilities would also be desirable for overall efficiency.

“Exchange rate appreciation in response to balance of payment surpluses would encourage reallocation of resources to the nontradables sector, thereby enhancing its vitality and further supporting rebalancing,” said the IMF.

The official press release can be accessed here.

You can stay up to date with the latest business and investment trends across Asia by subscribing to Asia Briefing’s complimentary update service featuring news, commentary, guides, and multimedia resources.

Related Reading

Singapore-European Union Conclude Free Trade Agreement

World Bank: Singapore and Hong Kong Best for Business

Singapore to Deepen Bilateral Relationship with China

Singapore Increases GDP Forecast

Singapore Tightens Employment Rules For Foreigners