Singapore and a number of other ASEAN countries offer favorable tax incentive schemes and concessions, aimed at attracting foreign investment. A number of Singapore’s DTAs include “tax sparing” provisions, which ensure that benefits granted to foreign investors under the source state’s tax incentive schemes will not be offset by the residence state’s taxes.

Under those provisions, the residence state treats the entity as if it had paid the usual corporate tax rate on that income in the source state, even when it has enjoyed a tax holiday or other concession. Essentially, the income is “spared” under the treaty in order to advance economic development. Currently, the countries with which Singapore has such agreements include Malaysia, Vietnam, the Philippines, Myanmar, Brunei, Canada and New Zealand.

Withholding Tax: Dividends

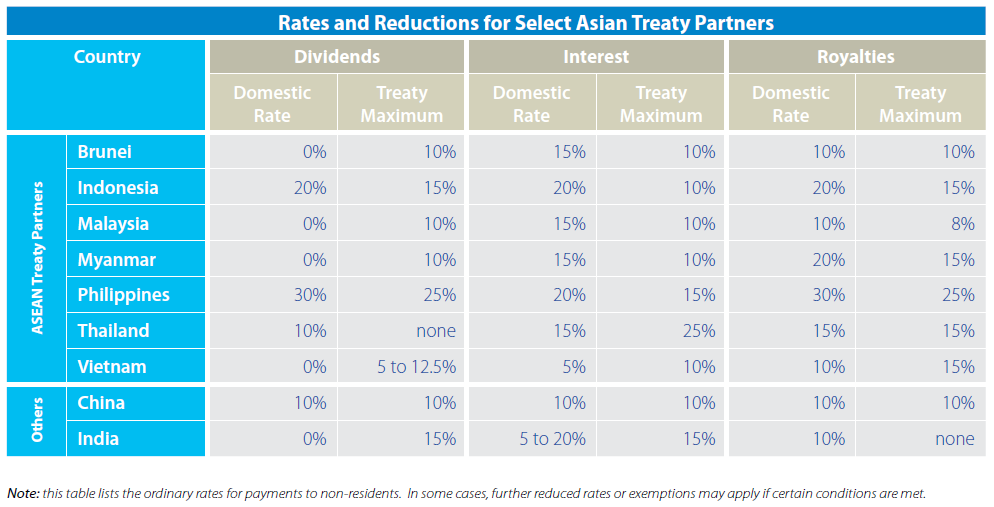

Singapore does not have a dividends tax under its one-tier corporate tax system, meaning that a Singaporean company’s after-tax profits can be distributed freely to both resident and non-resident shareholders without being subjected to further tax. A number of Singapore’s treaty partners do levy withholding taxes on dividends, however, and many DTAs reduce the rate that would otherwise be applicable under domestic laws.

Withholding Tax: Interest and Royalties

Tax treaties help to clarify the jurisdiction in which interest or royalties are deemed to arise. The source state will usually be the jurisdiction in which the payer of the interest or royalty is resident. In certain cases both states will tax interest or royalty income, although at lower rates. Singapore’s domestic withholding rate for interest and royalties derived by a non-resident through operations in Singapore is the prevailing corporate tax rate of 17 percent (or 20 percent in the case of individuals). For all other payments, the domestic withholding rates are 15 percent for interest and 10 percent for royalties.

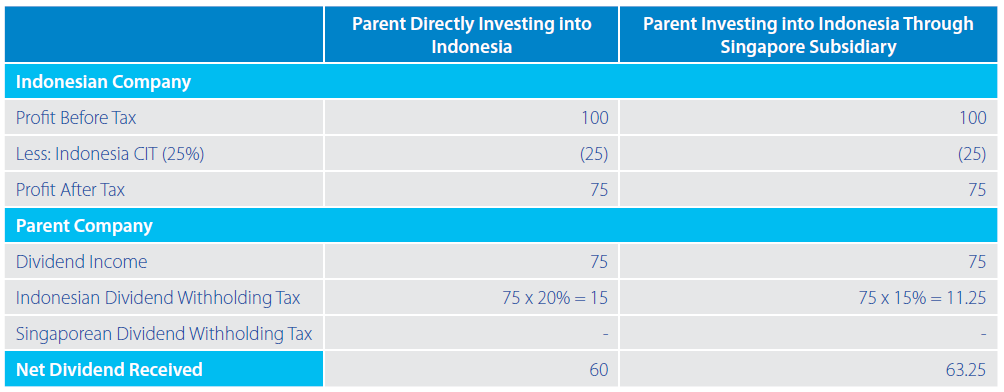

Routing Investment through Singapore

The example below shows how a business can save 5 percent in withholding tax by routing an investment in Indonesia through Singapore. When an Indonesian subsidiary tries to remit profits directly to its parent company, it is subject to Indonesia’s high 20 percent dividend withholding rate (assuming the parent company is located in a country that does not have a DTA with Indonesia providing for a lowered tax rate). By interposing a Singaporean holding company between the Indonesian company and ultimate parent, a business can avail itself of the lower 15 percent dividend withholding rate in the Indonesia—Singapore tax treaty. As Singapore does not impose withholding taxes on dividends, the Singaporean holding company can remit profits to its parent without incurring further withholding tax liability.

Singapore’s DTAs: Final Thoughts

Singapore’s extensive DTA network mitigates the problems of double taxation to a large extent. DTA considerations are essential to ensuring that a business operating across multiple jurisdictions can meet its tax obligations in those countries without suffering an excessive tax burden. Singapore’s favorable DTAs have been key in allowing it to retain its status as an international investment hub, by enabling companies to stay competitive with local businesses in Asia.

This article is an excerpt from the March issue of Asia Briefing Magazine, titled “The Gateway to ASEAN: Singapore Holding Companies.” In this issue, we highlight and explore Singapore’s position as a holding company location for outbound investment, most notably for companies seeking to enter ASEAN and other emerging markets in Asia. We explore the numerous FTAs, DTAs and tax incentive programs that make Singapore the preeminent destination for holding companies in Southeast Asia, in addition to the requirements and procedures foreign investors must follow to establish and incorporate a holding company.

This article is an excerpt from the March issue of Asia Briefing Magazine, titled “The Gateway to ASEAN: Singapore Holding Companies.” In this issue, we highlight and explore Singapore’s position as a holding company location for outbound investment, most notably for companies seeking to enter ASEAN and other emerging markets in Asia. We explore the numerous FTAs, DTAs and tax incentive programs that make Singapore the preeminent destination for holding companies in Southeast Asia, in addition to the requirements and procedures foreign investors must follow to establish and incorporate a holding company.

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email singapore@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

Related Reading

The Gateway to ASEAN: Doing Business in Singapore 2014 (Second Edition)

The Gateway to ASEAN: Doing Business in Singapore 2014 (Second Edition)

Dezan Shira & Associates’ Singapore business guide will provide readers with an overview of the fundamentals of investing and conducting business in Singapore. The 2014 edition explains the basics of company establishment, annual compliance, taxation, human resources, payroll and social insurance in the city-state, in addition to how a company established there can be used to conduct business in the wider ASEAN and Southeast Asian region.

First Cash-Dispensing Bitcoin ATM Launched in Singapore

Taiwan Signs Economic Partnership with Singapore

Singapore Tightens Employment Rules for Foreigners